Here are my top 10 ways that property investors can save tax

1 Property Investment Companies

- Restriction of Mortgage Interest Tax Relief – this doesn’t apply to companies

- Corporation Tax Rates – falling to 18% by 2020

- Capital Gains Tax – Capital Gains Tax indexation

- Stamp Duty – lower on share sales

- Inheritance Tax (IHT) and Potentially Exempt Transfers planning – better with shares

Further details in our blog http://stevejbicknell.com/2015/08/24/5-reasons-why-you-need-a-property-investment-company/

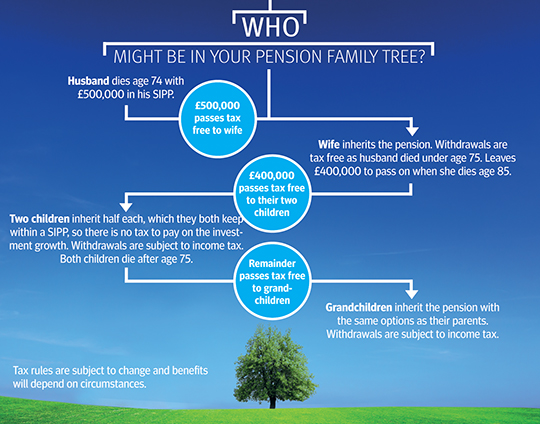

2 Commercial Property should be in a Pension Scheme

Self Invested Personal Pension (SIPP) Schemes and Small Self Administered Schemes (SSAS) can invest in commercial property, no tax on the rental income, no capital gains, you only pay tax when you draw your pension.

You also get tax relief on money paid into your Pension.

3 Claim tax deductible expenses

Claim allowable expenses

- Mortgage or Loan Interest (but not capital)

- Repairs and maintenance (but not improvements)

- Decorating

- Gardening

- Cleaning

- Travel costs to and from your properties for lettings or meetings

- Advertising costs

- Agents fees

- Buildings and contents insurance

- Ground Rent

- Accountants Fees

- Rent insurance (if you claim the income will need to be declared)

- Legal fees relating to eviction

If the property is furnished claim for Wear & Tear, you can claim 10% of the rent each year

Claim for repair and advertising expenses incurred in getting the property ready for renting

4 Use a Property Development Company to Save VAT

Property Development is a trade, where as Property Investment isn’t – renting out a residential property is a VAT exempt supply.

If you are planning significant building work, setting up a Development Company or using a building contractor might save VAT.

Assuming you employ a builder…

The VAT Rules are in VAT Notice 708 Buildings & Construction

Your builder may be able to charge you VAT at the reduced rate of 5 per cent if you are converting premises into:

- a ‘single household dwelling’

- a different number of ‘single household dwellings’

- a ‘multiple occupancy dwelling’, such as bed-sits, or

- premises intended for use solely for a ‘relevant residential purpose’

As your builder will be VAT registered, they reclaim the VAT they are charged and then charge you VAT at 5%.

If your business is property rental and you do the work yourself, you can’t take advantage of the 5% rate.

If your Development Company is VAT registered you can reclaim all the VAT.

Get your existing business or your property development company to convert the property and then sell it to another company that you own (may be an SPV) will be a VAT Zero Rated transaction. The other company then carries on the rental business.

5 Principle Private Residence Relief and Lettings Relief

Principle Private Residence Relief (PPR) is useful relief that saves you capital gains tax (18% for basic rate tax payers and 28% for higher rates tax payers) on your main residence.

You may also qualify for lettings relief after you have moved out.

6 Give away your Property in Stages

As long as the home you give away is your main home, Capital Gains Tax won’t be payable.

However, if you give away a second home, Capital Gains Tax may be payable if the property has increased in value between when you first owned it and when you gave it away.

If you sell your second home and give the money to your children, the gift won’t be included in your estate for Inheritance Tax purposes, provided you live for 7 years after you make the gift.

It is possible to to gift property in stages.

Your solicitor will draw up the required documents to conveyance a percentage of the property and register the transactions with the Land Registry.

In order to calculate the capital gain you will need to know the acquisition cost and any reliefs such as PPR.

Giving away your property in stages could save you from having to pay capital gains tax.

7 Claim Capital Allowances and Claim Tax Relief on Integral Features

FA2008 introduced a new classification of integral features of a building or structure, expenditure on the provision or replacement of which qualifies for WDAs at the 10% special rate. The new classification applies to qualifying expenditure incurred on or after 1 April 2008 (CT) or 6 April 2008 (IT).

http://www.hmrc.gov.uk/manuals/camanual/CA22300.htm

The rules on integral features apply where a person carrying on a qualifying activity incurs expenditure on the provision or replacement of an integral feature for the purposes of that qualifying activity. Each of the following is an integral feature of a building or structure –

- an electrical system (including a lighting system),

- a cold water system,

- a space or water heating system, a powered system of ventilation, air cooling or air purification, and any floor or ceiling comprised in such a system,

- a lift, an escalator or a moving walkway,

- external solar shading

Only assets that are on the list are integral features for PMA purposes; if an asset is not one of those included in the list, the integral features rules are not in point.

However, Plant and Machinery includes….

other building fixtures, such as shop fittings, kitchen and bathroom fittings

Many businesses have never claimed capital allowances for these items.

8 Consider Joint Ownership

If you own property personally you could double up your tax free Capital Gains Tax Allowance if you switch to owning property jointly with your spouse.

9 Check if you qualify for relief from ATED

Most residential properties (dwellings) are owned directly by individuals. But in some cases a dwelling may be owned by a company, a partnership with a corporate member or other collective investment vehicle. In these circumstances the dwelling is said to be ‘enveloped’ because the ownership sits within a corporate ‘wrapper’ or ‘envelope’.

ATED is a tax payable by companies on high value residential property (a dwelling).

There are reliefs that might lead to you not having to pay any ATED. You can only claim these by completing and sending an ATED return.

A dwelling might get relief from ATED if it is:

- let to a third party on a commercial basis and isn’t, at any time, occupied (or available for occupation) by anyone connected with the owner

- open to the public for at least 28 days per annum, if part of a property is occupied as a dwelling in connection with running the property as a commercial business open to the public, the whole property is treated as one dwelling and any relief will apply to the whole property

- part of a property trading business and isn’t, at any time, occupied (or available for occupation) by anyone connected with the owner

- part of a property developers trade where the dwelling is acquired as part of a property development business the property was purchased with the intention to re-develop and sell it on and isn’t, at any time, occupied (or available for occupation) by anyone connected with the owner

- for the use of employees of the company, for the company’s commercial business and where the employee does not have an interest (directly or indirectly) in the company of more than 10%, the employee’s duties must not include services for any present or future occupation of the property by someone connected with the company, the relief is also available where a partner in a partnership does not have an interest of more than 10% in the partnership

- a farmhouse, if it is occupied by a qualifying farm worker who farms the associated farmland, a former long-serving farm worker or their surviving spouse or civil partner

- a dwelling acquired by a financial institution in the course of lending

- owned by a provider of social housing

10 Take dividends this tax year

When you take dividends has never been more critical due to changes in the Summer Budget 2015, so if you have distributable reserves you might want to take more dividends this tax year, try our Dividend Calculator to see how much difference it could make.

Dividend tax rates before April 2016

| Tax band |

Effective dividend tax rate |

| Basic rate (20%) (and non-taxpayers) |

0% |

| Higher rate (40%) |

25% |

| Additional rate (45%) |

30.56% |

|

|

This will change from April 2016, see the table below

Dividend tax rates after April 2016

| Tax band |

Effective dividend tax rate |

| Tax Free £5,000 |

0% |

| Basic Rate Tax Payers (20%) |

7.5% |

| Higher Rate Tax Payers (40%) |

32.5% |

| Additional Rate Tax Payers (45%) |

38.1% |

The new rules are easier to follow, the 10% tax credit in the current rules is hard for most people to follow.

There is a Dividend Allowance factsheet which helps to explain how dividend tax will be calculated.

But be warned!

While these rates remain below the main rates of income tax, those who receive significant dividend income – for example due to very large shareholdings (typically more than £140,000) or as a result of receiving significant dividends through a closed company – will pay more.

So far we don’t know how much more!

steve@bicknells.net

{kind=link}