Download a copy – click here

Steve J Bicknell Tel 01202 025252

Helpful Comments on Tax and Finance – Bicknell Business Advisers Limited www.bicknells.net

We have prepared a report made up of 3 blogs written by Steve Bicknell and Whitney Highum

https://debitoor.com/blog/part-1-childminders-how-make-most-your-claims

https://debitoor.com/blog/part-2-childminders-what-know-about-new-scheme

https://debitoor.com/blog/part-3-parents-and-new-tax-free-childcare-scheme

The blogs cover childcare vouchers, salary sacrifice, the new 2017 scheme, and tax allowable expenses for childcare professionals. Click here to download

Tax-Free Childcare will be available to around 2 million households to help with the cost of childcare, enabling more parents to go out to work, if they want to, to provide greater security for their families.

In summary:

You find more details at Gov.UK

steve@bicknells.net

Childminders work in their own homes and are paid by parents for looking after their children, often while the parents are at work. Profits from childminding are usually chargeable to Income Tax as trade profits, although some occasional childminders’ profits may be chargeable as miscellaneous income.

Many childminders are members of the Professional Association for Childcare and Early Years (PACEY), formerly known as the National Childminding Association (NCMA). HMRC entered into an agreement with the NCMA on the expenses that will be allowed as deductions from childminding income.

Household expenditure

The agreement is based on the hours that childminders work and not on the number of children they care for. A childminder looking after a child on a full time basis for 40 or more hours each week is entitled to claim the full time proportion of expenses.

How this works is illustrated in the following table:

| Hours worked | % of Heating and lighting costs | % of Water rates, Council Tax and Rent |

| 10 | 8% | 2% |

| 15 | 12% | 4% |

| 20 | 17% | 5% |

| 25 | 21% | 6% |

| 30 | 25% | 7% |

| 35 | 29% | 9% |

| 40 (full time) | 33% | 10% |

The full time figures shown in the table should be scaled down from depending on hours worked.

Wear and tear of household furnishings

A deduction of 10% of total childminding income may be made to cover the wear and tear of furniture and household items. This is intended to include household items which are not used wholly and exclusively in childminding. A childminder claiming this deduction may not, however, claim relief for the cost of replacing such household items. Reasonable costs of cleaning household items where the need for cleaning is as a result of childminding activities may be allowed as a separate item.

The agreement also covers the following expenditure:

Food and drink

Reasonable estimates for the costs of food and drink provided for the children being cared for are acceptable and receipts are not required.

Car expenses

Where appropriate, childminders can use the simplified expenses mileage rates. However, if the childminder wishes, the actual cost of car expenses for childminding purposes can be claimed instead.

Other costs

Also allowable – the cost of toys, outings, books, safety equipment, stationary, travel fares, membership fees or subscriptions to your childminding organisation, public liability insurance premiums and the actual cost of telephone use for childminding purposes.

You can find further details in BIM52751

steve@bicknells.net

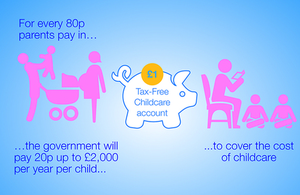

The Government wants to help working families and currently if you are an employee your employer can help with childcare and could for example buy childcare vouchers of up to £55 per week, the vouchers would be a tax free benefit to the employee. However, if you’re self employed you aren’t an employee so the rules don’t apply.

So recently there has been a consultation on what should be be done in the future.

The key proposals are:

The chart below shows how it should work:

steve@bicknells.net

Salary Sacrifice is a very tax efficient way to give your employees benefits and the most popular benefits are Pensions and Childcare. I wrote a blog back in 2011 which explained how it can save 45.8% in tax and NI

HMRC decided on 9th April 2013 that it was time to “clarify” in their Manuals what are successful and unsuccessful salary sacrifice schemes and have added some further guidance. Their Staff are instructed not to approve schemes (Employment Income Manual EIM42772)….

You (HMRC) may get requests for advice:

- on how to set up a salary sacrifice arrangement, or

- on whether draft documentation will achieve a successful salary sacrifice.

You (HMRC) should not comment on either of these areas. Salary sacrifice is a matter of employment law, not tax law. The nature of an employee’s contract of employment is a matter for the employer and employee.

The specific updates are:

EIM42750 – Salary Sacrifice – updated – this contains the examples of schemes

EIM42777 – Contractual arrangements – this has interesting comments on childcare and pensions

EIM42778 – Exemption from Tax/NIC – basically stating that exemption may require that the sacrifice may be available to all employees but that the sacrifice must not reduce the employees wages below National Minimum Wages

The following is an example of an unsuccessful Childcare Salary Sacrifice:

The pay slip for the month ended 31 July 2006 gives monthly pay as £2000 plus overtime of £100, deductions for tax of £355 and NIC. The pay slip for the following month shows monthly pay of £2000 plus overtime of £100, deductions for NIC, childcare vouchers of £200 and tax of £310. The code number operated on the salary has not changed.

The situation is not clear from the payslip. When asked, the employer explains that for August, because childcare vouchers of £55 a week are exempt, £220 of vouchers has been deducted from the gross pay of £2100 and tax charged on the net figure of £1880. Further information is needed, for example a copy of the employment contract and any variations agreed by the employer and employee to that contract.

It is established that in July the employee bought childcare vouchers. The employer was not involved. The employer accepts that as the childcare in July was not provided by him, no tax exemption is available. In August the employee asked the employer to buy the childcare vouchers to take advantage of the exemption. The employer did this and deducted the cost from the monthly salary. The contract of employment shows that the employee is entitled to a base salary of £24000 to be paid monthly. This contract has not been varied. As the employee’s entitlement has remained the same, this is not a successful sacrifice. (See EIM42766).

If you operate salary sacrifice schemes its worth checking that your schemes comply, the tax consequences of failure to comply could be substantial.

steve@bicknells.net

Most employees pay 20% tax, 12% Ees NI and their employer pays 13.8% NI, so thats a total tax of 45.8% on employment income.

There are a range of tax and NI free benefits, for example childcare vouchers, where £55 per week can be paid by the employer, so lets use that as an example, using the calculator

http://listentotaxman.com/index.php

An employee earning £30k a year gets

| Wage Summary | Yearly | Monthly | Week |

| Gross Pay | £30,000.00 | £2,500.00 | £576.92 |

| Tax free Allowances | £7,475.00 | £622.92 | £143.75 |

| Total taxable | £22,525.00 | £1,877.08 | £433.17 |

| £4,505.00 | £375.42 | £86.63 | |

| National Insurance | £2,732.64 | £227.72 | £52.55 |

| Total Deductions | £7,237.64 | £603.14 | £139.19 |

| Net Wage | £22,762.36 | £1,896.86 | £437.74 |

| Employers NI | £3,164.06 | £263.67 | £60.85 |

Total Tax and NI = £10401.70

If they use Salary Sacrifice for £55 x52 = £2860, new salary would be £27140

| Wage Summary | Yearly | Monthly | Week |

| Gross Pay | £27,140.00 | £2,261.67 | £521.92 |

| Tax free Allowances | £7,475.00 | £622.92 | £143.75 |

| Total taxable | £19,665.00 | £1,638.75 | £378.17 |

| £3,933.00 | £327.75 | £75.63 | |

| National Insurance | £2,389.44 | £199.12 | £45.95 |

| Total Deductions | £6,322.44 | £526.87 | £121.59 |

| Net Wage | £20,817.56 | £1,734.80 | £400.34 |

| Employers NI | £2,769.38 | £230.78 | £53.26 |

Total Tax and NI = £9091.82

A saving of £1309.98 (45.8% of £2860)

For saves on this scale should you be looking at Salary Sacrifice schemes for your employees,I have seen schemes where it can be applied to a wide variety of things from Pensions to Cars

steve@bicknells.net

{kind=link}