First lets have a recap on why Pensions are a fantastic investment and a great way to save tax.

Inheritance Tax

IHT only applies if the pension company has to pay the value of your scheme to your estate, in which case it becomes like any other asset, but generally the pension pot is held in a discretionary trust, which means it isn’t taxed on death.

You can now nominate anyone not just dependents to be the beneficiary.

Since 6th April 2015 anyone who inherits a pension fund from a person who dies before the age of 75 is entitled to receive it tax free and the you can take the money as a lump sum or income. Once over 75 a special tax of 45% applies (previously 55%), you could reduce this by taking a regular income. The tax rate should drop again in April 2016.

Business Premises

Your pension can own Commercial Property, including your own business premises.

In many cases it is better for business premises to be owned by the business owners pension fund because:

- The object of the business is not to own its own property, the objective should be for the business to make profits from trading

- The business could use cash tied up in the premises to invest in trading activities

- Pensions are a very tax efficient method of ownership – no capital gains, no tax on rental profits

- Company Pension Contributions are Tax Deductible and Individual contributions get income tax refunds

- You may be able to use 3 year Carry Forward to get funds into your pension scheme

Commercial Investment Property

Your pension scheme can own commercial investment property – shops, offices, industrial units.

It can borrow up to a third of the value of the pension scheme.

There is no capital gains tax and no tax on the rental income.

In Specie Transfers

In Specie transfers can be used to move assets into your pension scheme this could incur capital gains and SDLT (Stamp Duty), but you will benefit from tax relief as if you had paid in cash. Currently that means at tax relief of between 20% and 45%.

Once the assets are in a pension scheme transfers ‘in specie’ between schemes are tax free (no capital gains) and no SDLT.

HMRC say…

In our view the assumption by the transferee fund or by the trustees of the transferee fund, of obligations to provide benefits is not chargeable consideration.

Net Relevant Earnings (NRE)

Many owner managed businesses only pay small salaries and take large dividends, this would normally restrict the level of pension contributions allowed, however, their companies can pay the maximum allowed – currently £40k per year.

Employer v’s Employee Pension Payments (Net Relevant Earnings)

Lend Money to your Pension Scheme

If you have a SSAS or a SIPP Pension you will probably want to invest some of your funds in Commercial Property – Shops, Office, Industrial Units. Pension funds can borrow money and with the current interest rates low and yields as high as 10%, you can increase your return and use less cash by borrowing.

But one thing you may not know is that connected parties can lend to the fund…

Trustees of registered pension schemes may sometimes wish to borrow funds, for example to enable them to purchase an asset. There is no objection to a registered pension scheme borrowing funds for any purpose providing that the scheme administrator/trustees are satisfied that the borrowing will benefit the scheme and that the borrowing is within the rules laid down by the Department for Work and Pensions (DWP).

A registered pension scheme is treated as borrowing or having a liability of an amount, if that amount is to be repaid or met from cash or assets held for the purposes of the pension scheme.

A registered pension scheme may borrow funds from any individual, company or financial institution whether or not they are connected to the scheme, but any borrowing from a connected party which is not made on commercial terms will be subject to a tax charge – see RPSM04104020 .

http://www.hmrc.gov.uk/manuals/rpsmmanual/rpsm07104010.htm

This is useful where you have paid in the maximum allowed pension contributions but you still have cash, so you could lend to your pension to buy a property.

25% Tax Free

When you retire you get 25% of you pension fund tax free.

http://www.pensionsadvisoryservice.org.uk/about-pensions/saving-into-a-pension/pensions-and-tax/tax-and-the-cash-lump-sum

Shares and Loans

SSAS Pensions can lend money to their scheme employer and the scheme employer can borrow from a SSAS subject to passing 5 tests.

Pensions can even buy shares in your business.

Family Pension Schemes

So now you can see why Pensions are brilliant! lets look at Family Pensions…

Rowanmoor Group PLC summarise the benefits of a Family SIPP as follows

The potential benefits of the Family Pension Trust are:

- Members, including minors, can pool funds together to benefit from a wider range of investment opportunities

- Multiple common investment funds allow a variety of bespoke portfolios to be established for some or all members, which widens investment options and can reduce costs

- Investment decisions do not have to be unanimous

- Different attitudes to risk can be catered for

- No minimum fund requirement

- Increased borrowing potential

- Succession planning options and death benefits

- Comprehensive, flexible options to enable retirement income to be phased

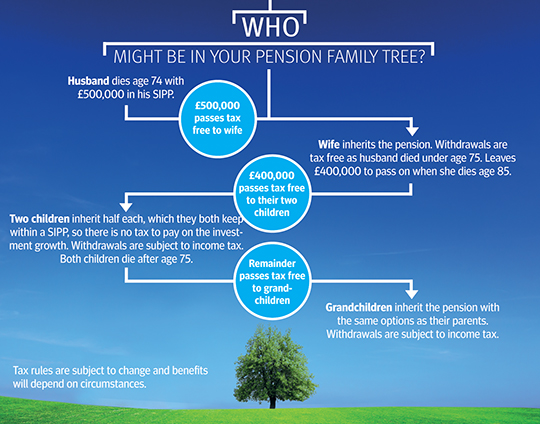

Hargreaves Lansdown have a very helpful article on their Family SIPP which includes this example

http://www.hl.co.uk/__data/assets/image/0005/8740085/Pension-family-tree.jpg

Please note – always take professional advice from qualified professionals before setting up a pension, making investment decisions and transferring assets

steve@bicknells.net

{kind=link}