Actually, this isn’t a blog about the Mona Lisa its actually about Lifetime Investment Savings Accounts (LISA).

LISA’s are available from April 2017 and are a retirement saving option.

Save up to £4000 per year

You must be aged between 18 and 40

Anything paid in will be topped up by 25% at the age of 50

Over the age of 60 you can take out all the money tax free

If you take it before 60 you lose the 25% bonus and get a 5% charge

Personally, I don’t think they sound great, if you want to save for retirement why not just save in a pension?

If you want to save in a bank why not just use the Personal Savings Allowance which started in April 2016.

The PSA will apply to all non-ISA cash savings and current accounts, and will allow some savers to receive a generous portion of their interest totally free of tax.

Its expected that 95% of savings will no longer be taxed.

Basic rate taxpayers will receive £1,000 in savings income tax free, higher rate taxpayers get a band of £500 and additional rate tax payers get nothing.

The Budget announced that from 6 April 2017 any adult under 40 will be able to open a new Lifetime ISA. They can save up to £4,000 each year and will receive a 25% bonus from the government on every pound they put in.

This is why you should get one!

25% Bonus – free money is always good

It encourages you to save – building up savings for a house or retirement will definitely be of benefit

The under 40’s will probably see this as better than a pension plan, as you can’t access pensions until you are 55

Personally Pensions are still my favourite…

Lets say you invest £10,000 per year of earned gross income, increasing each year by 3% for inflation and see the effect of tax relief at 40% and 20%, assuming a return on the investment of 7% (which you should get with Commercial Property Investment)

40% Tax Rate

20% Tax Rate

Year

Pension

No Pension

% Diff

Year

Pension

No Pension

% Diff

1

£10,700

£6,252

71%

1

£10,700

£8,336

28%

2

£22,470

£12,954

73%

2

£22,470

£17,272

30%

3

£35,395

£20,131

76%

3

£35,395

£26,841

32%

4

£49,564

£27,808

78%

4

£49,564

£37,078

34%

5

£65,077

£36,013

81%

5

£65,077

£48,017

36%

6

£82,036

£44,773

83%

6

£82,036

£59,698

37%

7

£100,555

£54,119

86%

7

£100,555

£72,158

39%

8

£120,754

£64,081

88%

8

£120,754

£85,441

41%

9

£142,761

£74,692

91%

9

£142,761

£99,590

43%

10

£166,715

£85,987

94%

10

£166,715

£114,649

45%

11

£192,765

£98,000

97%

11

£192,765

£130,667

48%

12

£221,070

£110,771

100%

12

£221,070

£147,694

50%

13

£251,801

£124,337

103%

13

£251,801

£165,782

52%

14

£285,140

£138,740

106%

14

£285,140

£184,987

54%

15

£321,285

£154,024

109%

15

£321,285

£205,365

56%

16

£360,445

£170,233

112%

16

£360,445

£226,978

59%

17

£402,846

£187,416

115%

17

£402,846

£249,888

61%

18

£448,731

£205,621

118%

18

£448,731

£274,161

64%

19

£498,358

£224,901

122%

19

£498,358

£299,868

66%

20

£552,006

£245,309

125%

20

£552,006

£327,079

69%

Even when you consider:

Your money is locked up till you are 55

You pay tax when you take money out of the pension

You can get 25% out of the pension tax free

The difference in growth is massive

If you do salary sacrifice you can increase the tax effect by saving national insurance too.

The Government like Crowdfunding and Peer-to-Peer Lending, so in April 2016 the Innovative Finance ISA is being introduced.

In summary, its aim is to increase the number of loans available through crowdfunding by giving a tax incentive to those providing the money. There is greater risk for investors as their investments won’t be brought into the Financial Services Compensation Scheme but the returns for investors will be much higher than traditional savings accounts.

Innovative Finance ISAs are expected to be available from 6 April directly through peer-to-peer lending platforms such as Zopa, Ratesetter and Funding Circle, or via selected fund platforms. They will have the same annual savings limit as regular ISAs, £15,240.

most pensions, including state pensions, company and personal pensions and retirement annuities

interest on savings and pensioner bonds

rental income (unless you’re a live-in landlord and get £4,250 (£7,500 from April 2016) or less)

benefits you get from your job

income from a trust

dividends from company shares

So how can you pay less income tax?

Here are 10 suggestions…

Pension

When you pay into a pension you get income tax relief on your contributions .

Lets say you invest £10,000 per year of earned gross income, increasing each year by 3% for inflation and see the effect of tax relief at 40% and 20%, assuming a return on the investment of 7% (which you should get with Commercial Property Investment)

40% Tax Rate

20% Tax Rate

Year

Pension

No Pension

% Diff

Year

Pension

No Pension

% Diff

1

£10,700

£6,252

71%

1

£10,700

£8,336

28%

2

£22,470

£12,954

73%

2

£22,470

£17,272

30%

3

£35,395

£20,131

76%

3

£35,395

£26,841

32%

4

£49,564

£27,808

78%

4

£49,564

£37,078

34%

5

£65,077

£36,013

81%

5

£65,077

£48,017

36%

6

£82,036

£44,773

83%

6

£82,036

£59,698

37%

7

£100,555

£54,119

86%

7

£100,555

£72,158

39%

8

£120,754

£64,081

88%

8

£120,754

£85,441

41%

9

£142,761

£74,692

91%

9

£142,761

£99,590

43%

10

£166,715

£85,987

94%

10

£166,715

£114,649

45%

11

£192,765

£98,000

97%

11

£192,765

£130,667

48%

12

£221,070

£110,771

100%

12

£221,070

£147,694

50%

13

£251,801

£124,337

103%

13

£251,801

£165,782

52%

14

£285,140

£138,740

106%

14

£285,140

£184,987

54%

15

£321,285

£154,024

109%

15

£321,285

£205,365

56%

16

£360,445

£170,233

112%

16

£360,445

£226,978

59%

17

£402,846

£187,416

115%

17

£402,846

£249,888

61%

18

£448,731

£205,621

118%

18

£448,731

£274,161

64%

19

£498,358

£224,901

122%

19

£498,358

£299,868

66%

20

£552,006

£245,309

125%

20

£552,006

£327,079

69%

Even when you consider:

Your money is locked up till you are 55

You pay tax when you take money out of the pension

You can get 25% out of the pension tax free

The difference in growth is massive

If you do salary sacrifice you can increase the tax effect by saving national insurance too.

2. ISA

Individual Savings Accounts have been around for a few years and very soon the Help to Buy ISA will be launched

Top 10 facts and rules…

Its only available to ‘First Time Buyers’

‘First Time Buyers’ can only have one Help to Buy ISA with one provider

You can pay in £1,000 when you open the account and then save a maximum of £200 per month

The maximum government bonus is £3,000 (but you can lower amounts of bonus if you have less than £12,000)

The scheme will run for 4 years from the date it opens (Autumn 2015)

Couples can have a Help to Buy ISA each which means if they don’t want to wait 4 years could save £12,000 in 25 months where as a single saver would need 55 months

Unlike ISA’s where you open one per year, the Help to Buy ISA will continue for 4 years

You can withdraw funds but if its not to buy a home then you won’t get the bonus

More than 100,000 homes have now been bought with government backed schemes

You will be able to get them at banks and building societies

3. Salary Sacrifice

Salary Sacrifice is a very tax efficient way to give your employees benefits and the most popular benefits are Pensions and Childcare. I wrote a blog back in 2011 which explained how it can save 45.8% in tax and NI

HMRC decided on 9th April 2013 that it was time to “clarify” in their Manuals what are successful and unsuccessful salary sacrifice schemes and have added some further guidance. Their Staff are instructed not to approve schemes (Employment Income Manual EIM42772)….

You (HMRC) may get requests for advice:

on how to set up a salary sacrifice arrangement, or

on whether draft documentation will achieve a successful salary sacrifice.

You (HMRC) should not comment on either of these areas. Salary sacrifice is a matter of employment law, not tax law. The nature of an employee’s contract of employment is a matter for the employer and employee.

The specific updates are:

EIM42750 – Salary Sacrifice – updated – this contains the examples of schemes

EIM42777 – Contractual arrangements – this has interesting comments on childcare and pensions

4. Employment Expenses

As an employee you can claim tax relief for expenses incurred in doing your job, for example business mileage, cycling on business, hotels, meals, business phone calls, in fact anything as long as its business related

If your claim is less than £2500 you can make your claim using Form P87 http://www.hmrc.gov.uk/forms/p87.pdf if its more than £2500 you will need to complete a Self Assessment Return (you need to phone HMRC to request a Self Assessment Return – contact details below), if you know your UTR number you can register and file your Self Assessment Return on line.

5. Dividends

When you take dividends has never been more critical due to changes in the Summer Budget 2015, so if you have distributable reserves you might want to take more dividends this tax year, try the Dividend Calculator above to see how much difference it could make.

6. Tax break for Couples

A new tax break as launched this week from 6 April 2015, which will be eligible to more than 4 million married couples and 15,000 civil partnerships.

The Allowance means a spouse or civil partner who doesn’t pay tax – therefore is not earning at all or is earning below the basic rate threshold (£10,600) – can transfer up to £1,060 of their personal tax-free allowance to a spouse or civil partner – as long as the recipient of the transfer doesn’t pay more than the basic rate of income tax.

7. Tax Free Benefits

Getting tax free benefits will save you lots of tax, here some ideas…

Pensions – Up to £40k can be paid in to you pension scheme by your employer (2015/16) and you can use carry forward to pay in even more

Childcare – Up to £55 per week but check the rules to makesure your childcare complies (HMRC Leaflet IR115) – these rules are changing soon.

Your Personal Allowance goes down by £1 for every £2 that your adjusted net income is above £100,000. This means your allowance is zero if your income is £121,200 or above.

9. Green Company Car

A calculator is available here: http://www.hmrc.gov.uk/calcs/cars.htm and rates are shown in the table below for zero emission vehicles and some of the lower CO2 vehicles.

10. Check your P800

The P800’s are likely to contain errors because:

Large amounts of data are manually input

Estimates especially for Bank Interest and Investment Income

So check the following carefully:

P60 – you get this at the end of each tax year

P45 – you get this when you leave a job

PAYE Coding Notice

P11D Expenses and benefits

P9D Expenses payments and income from which tax cannot be deducted

Bank and Building society statements

Pension Tax Deductions

Its expected that around 3 million people will be asked to pay more tax and around 2 million people will have overpaid.

Housing and home ownership are a top priority in the UK and last week new proposals were announced in the Productivity Plan (see page 11 section 9)

The UK has been incapable of building enough homes to keep up with growing demand. This harms productivity and restricts labour market flexibility, and it frustrates the ambitions of thousands of people who would like to own their own home. The government will:

introduce a new zonal system which will effectively give automatic permission on suitable brownfield sites

take tougher action to ensure that local authorities are using their powers to get local plans in place and make homes available for local people, intervening to arrange for local plans to be written where necessary

bring forward proposals for stronger, fairer compulsory purchase powers, and devolution of major new planning powers to the Mayors of London and Manchester

extend the Right to Buy to housing association tenants, and deliver 200,000 Starter Homes for first time buyers

restrict tax relief to ensure all individual landlords get the same level of tax relief for their finance costs

Automatic planning consent on Brownfield sites, when approved, follows a number of other important incentives such as the Starter Homes initiative 20% discount.

The 20% discount is achieved by waiving local authority fees for homebuilders of at least £45,000 per dwelling on brownfield sites.

At the heart of the Starter Homes initiative is a change to the planning system. This will allow house builders to develop under-used or unviable brownfield land and free them from planning costs and levies. In return, they will be able to offer homes at a minimum 20% discount exclusively to first time buyers, under the age of forty. Under the proposals, developers offering Starter Homes would be exempt from those Section 106 charges and Community Infrastructure Levy charges. The homes could then not be re-sold at market value for a fixed period – making sure that the savings are passed onto homebuyers.Gov.uk

To qualify first time buyers must be under the age of 40 and living in England.

Also the Help to Buy ISA for first time buyers where they could qualify for a £3,000 bonus

There is also the Help to Scheme where home buyers may only need a 5% deposit

With a Help to Buy: equity loan the Government lends you up to 20% of the cost of your new-build home, so you’ll only need a 5% cash deposit and a 75% mortgage to make up the rest.

You won’t be charged loan fees on the 20% loan for the first five years of owning your home.

‘First Time Buyers’ can only have one Help to Buy ISA with one provider

You can pay in £1,000 when you open the account and then save a maximum of £200 per month

The maximum government bonus is £3,000 (but you can lower amounts of bonus if you have less than £12,000)

The scheme will run for 4 years from the date it opens (Autumn 2015)

Couples can have a Help to Buy ISA each which means if they don’t want to wait 4 years could save £12,000 in 25 months where as a single saver would need 55 months

Unlike ISA’s where you open one per year, the Help to Buy ISA will continue for 4 years

You can withdraw funds but if its not to buy a home then you won’t get the bonus

More than 100,000 homes have now been bought with government backed schemes

You will be able to get them at banks and building societies

A first-time buyer is someone who does not and has never owned an interest in a residential property, either inside or outside the UK.

Many people have said “I owned a property previously but now rent”, “I have a shared ownership property” or “I have inherited a property” can I still open a Help to Buy ISA? And the answer is NO – you have to be a first-time buyer to open one.

The limits for Junior ISAs and Child Trust Funds have already been increased from £3,700 to £4,000.

From July, restrictions on corporate bonds and gilts will have the 5 year rule removed allowing you to invest in short dated securities such as Retail Bonds.

There are plans to enable Peer-to-Peer loans to be held in NISA’s but that’s still in the consultation stage.

Between now and July the most you can invest in an Cash ISA is £5,940.

Tax Relief on Charity Donations – Are you using Gift Aid? are you a higher rate tax payer entitled to additional relief?

Saving on Inheritance Tax – Many people don’t have a Will let alone any IHT planning!

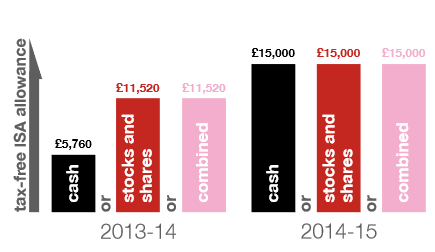

Making Use of ISA’s – Why get taxed on the interest on your savings if you could have an ISA? Its easy to get an ISA and you can still have access to your ISA savings if you need it, the current ISA allowance is £11,520 or £5,760 for cash ISA’s

Avoiding tax penalties and late filing – This just requires you to be organised, make sure you know the filing dates http://www.hmrc.gov.uk/sa/deadlines-penalties.htm and get the information needed in plenty of time

Savings on Capital Gains – The current allowance for 2013/14 is £10,900 (previously £10,600) for an individual many people seem to forget they have this allowance

Income Tax and Personal Allowances – Consider who should own assets (and get income from those investments) – you or your spouse – so that you can minimise your tax liability

Many parents, grandparents and other family members like to save for children but are you paying tax on the interest?

The £100 Rule

HMRC Form R85 is used to claim interest tax free but what you might not realise is that despite your child having a personal tax allowance from birth there is a maximum of £100 per year which can earned tax free in interest and dividends earned on parental/family gifts.

So for 2 parents that’s £200 plus grandparents have the same exemption, but if the interest exceeds the limit even by a small amount, the exemption is lost and whole amount of interest becomes taxable.

Junior ISA

Children can have an ISA in their name, the maximum annual contribution limit is £3,720 (2013/14) in cash or shares but the money will be locked in until the child is 18. The £100 rule doesn’t apply to ISA’s.

Pension

Yes, crazy as it might sound your baby can start a pension plan.

You can receive 20% tax relief even if you don’t pay tax. The maximum you can contribute is £3,600 gross – a payment of £2,880 to which the taxman adds £720. This is the case even for people who don’t pay tax, such as children and non-earning spouses.

{kind=link}